- So, this is adulting by DoitDuit

- Topics

- Stock Analysis

Stock Analysis

Worst Profit in >10 Years, but Rises 4% the Next Day

Net profit was dragged down by write-offs and FOREX losses. But management has a plan for value unlocking, disposing non-core assets, and exiting loss-making segments. Management projects up to RM3 billion in capital returns in the next 3 years if their plans are successful.

The next bottleneck in AI: Power Semiconductor

AI agent is the AI inflection point, creating huge demand for computing and power. Power semi is the next bottleneck if AI data centers are forced to transition to 800VDC. One high risk bet may benefit from this transition.

IJM: Tactical Opportunity to Ride on DC Boom Plus Value Unlocking Exercises

IJM looks like a catalyst story in the making. The failed Sunway takeover may have become the trigger that forces management to unlock hidden value through asset disposals, potential spin-offs, and special dividends, while its construction arm continues to ride the data center boom.

US vs China AI; and Stocks at 52W Low

While the US burns billions chasing AGI, China is weaponizing cheap AI to dominate global distribution. As tech valuations soar, AI bubble risks echo the dot-com crash. Smart investors are looking elsewhere: scooping up elite, undervalued businesses currently trading at 52-week lows. Is your portfolio prepared for what's next?

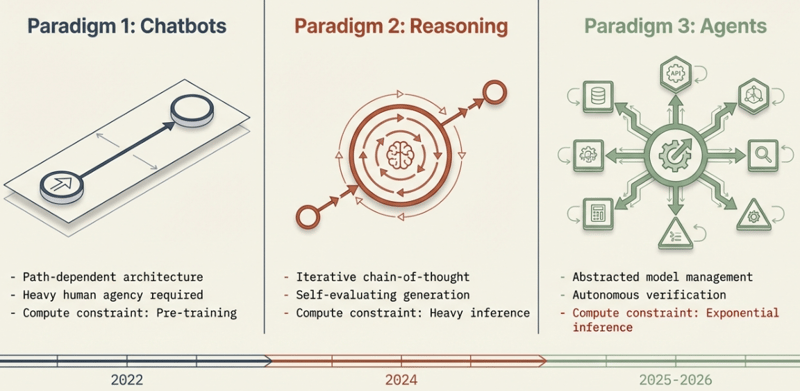

AI Inflection Point: AI Agents, Value Creation Process & Business Model

AI is rapidly evolving from simple chatbots to autonomous agents, unlocking unprecedented productivity and massive computing demands. This shift is disrupting traditional value creation and business models.

Dutch Lady FY25 Review: Strong Performance; FY26 will be Full Year of New Plant Operation

Dutch Lady Hits Record High Yearly and Quarterly Revenue but Profit dragged by Tax provisions. Outlook remains positive as FY2026 will see the full benefits of their 6-year CAPEX being realized. Middle East crisis is expected to raise costs, but near-term supplies remain secured and manageable. Cost impact may be seen in 2H2026, but the situation is still fluid.